Introduction

The AI industry has entered its most dangerous phase yet: the moment when hype collides with capital reality. Billions of dollars have been poured into large language models and infrastructure with the promise of transformative returns. Yet beneath the headlines, a quieter truth is emerging: different regions are pursuing fundamentally different capital strategies, and only one model shows clear signs of long-term sustainability.

- US Pure-Plays Face Capital Urgency: OpenAI, Anthropic, and xAI operate at 0.30x to 16.7x CapEx-to-revenue ratios that become unsustainable beyond 1–2 years without major revenue acceleration or consolidation.

- Hyperscalers Already Won: Microsoft, Google, Meta, and Apple leverage AI to strengthen existing revenue streams (Azure, Cloud, ads, hardware) rather than betting on AI as standalone products. This structural advantage is permanent.

- China Wins on Cost, Not Technology: Government subsidies reduce effective CapEx by 30–40%, enabling ByteDance and Alibaba to achieve 90% of US AI performance at dramatically lower cost structures.

- India's Services Firms Are Uncorrelated Winners: TCS, Infosys, and HCLTech profit from enterprise AI implementation at 60–70% labor cost advantage. This gap is structural and won't compress.

- Geographic Winners Are Clear: Hyperscalers (US), subsidized players (China), and services arbitrage (India) dominate. Europe and Japan lack equivalent structural advantages and become acquisition targets.

- The 2026–2027 Reorganization Is Inevitable: Down rounds in Q2–Q3 2026, funding winter in Q4–2027, and consolidation through 2027. Pure-play independence becomes rare by end of 2027.

- Capital Structure Now Trumps Technology: The winners are determined by sustainable funding, geographic policy advantages, and labor arbitrage, not raw algorithmic brilliance.

- For Builders: Vertical AI applications beat general models. India-based engineering teams become permanent capital efficiency. Independence in model building should not be the exit assumption.

This report maps the global AI capital landscape as of March 2026. Using public filings, earnings data, and analyst estimates, we identify four distinct capital models competing for dominance: US pure-play AI companies, US hyperscalers, China’s state-backed players, and India’s services-driven approach.

The conclusion is uncomfortable but necessary: most pure-play AI companies are burning cash at rates they cannot sustain. The winners will not be the companies with the most impressive demos or the highest valuations. They will be the ones with sustainable capital structures, geographic advantages, and realistic paths to profitability.

The delusion is ending. The next 18–24 months will separate the serious players from the hype machines.

Executive Summary

The AI industry is not experiencing one bubble. It’s running four completely different capital experiments at once, and only one of them will survive.

Genuine News Deserves Honest Attention.

High-conviction projects require an intelligent audience. Connect with readers who value sharp reporting.

👉 Submit Your PR- US Pure-Plays (OpenAI, Anthropic, xAI) are burning through cash at rates that don’t make sense long-term. We’re talking 2-to-16x CapEx-to-revenue ratios. By 2027, most will either consolidate, secure major partnerships, or face extinction.

- US Hyperscalers (Microsoft, Google, Meta, Apple) have already won. They’re not betting on AI replacing their core business. They’re using AI to strengthen it. That’s a structural advantage no startup can compete with.

- China’s State-Backed Players (Alibaba, ByteDance, Tencent) are winning on cost, not technology. Government subsidies reduce their effective CapEx by 30–40%. This is ruthless but straightforward capital structure arbitrage.

- India’s Services Firms (TCS, Infosys, HCLTech) are quietly printing money. They don’t care which AI model wins globally. They profit by helping enterprises adopt whatever wins, at massive labor cost advantages.

The math is brutal. The winners are determined by geography and capital structure, not raw technological brilliance.

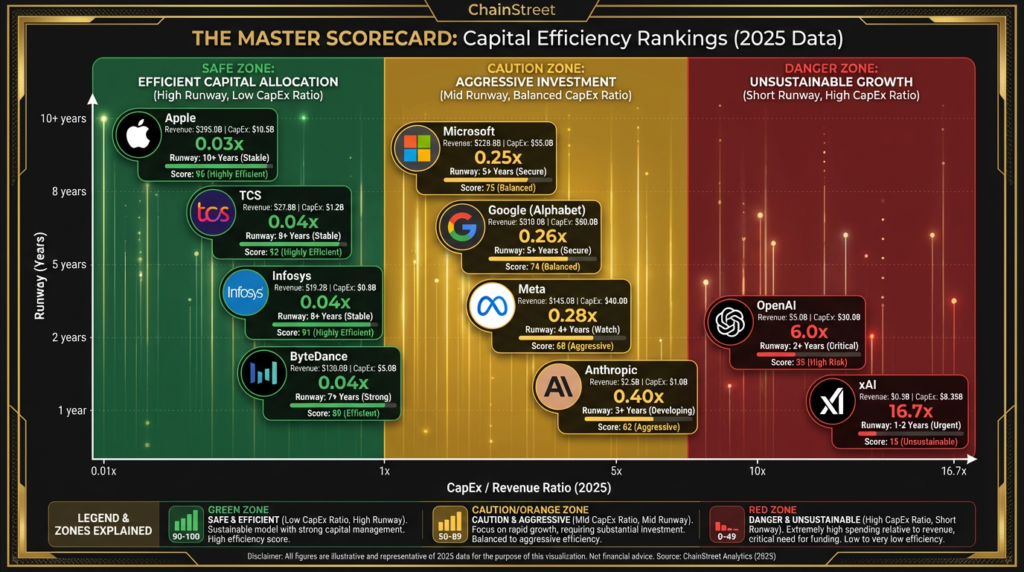

The Master Scorecard (2025 Data)

Key Data Points

*China figures include government subsidies reducing effective CapEx by 30-40% (Jefferies Research) **Estimated figures as of early 2026

The dividing line: Companies below 0.40x CapEx/Revenue with solid revenue are sustainable. Above 0.70x? You’re running on investor faith, not fundamentals.

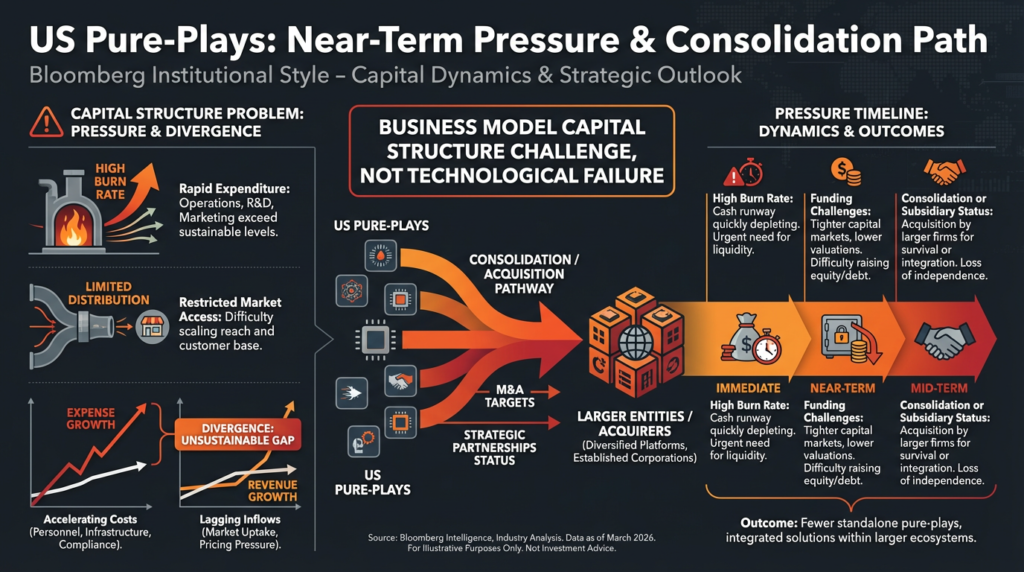

US Pure-Plays: The Math Doesn’t Work

Start with OpenAI. The company generated roughly $4–5 billion in revenue in early 2026, while burning through $10+ billion in estimated annual CapEx. That’s a 2x ratio. Gross margins sit around 33%, which means for every dollar in revenue, 67 cents evaporates before you even count operating costs. To reach break-even, revenue needs to grow 3–5x. In a commoditizing market with dozens of competing models and pricing pressure? Good luck.

Anthropic’s situation is different but equally constrained. The company spent $2.66 billion on AWS infrastructure in just nine months of 2025. Q3 revenue was $2.55 billion. They’ve committed to $80 billion in cloud spending through 2029. That’s a massive bet on exponential revenue growth that may never materialize. If growth slows, this becomes a funding crisis, not a business problem.

xAI operates under different constraints because Elon built owned infrastructure (Colossus data centers) instead of renting cloud capacity. That creates long-term optionality. But right now, the numbers are stark: $5 billion+ in annual CapEx on $0.3 billion in revenue (estimated). For a 2-year-old startup, that’s appropriate. The problem is competing directly against Microsoft, Google, and Meta while trying to build independent distribution. That’s an asymmetric fight.

Three paths forward exist. None are attractive:

- Accelerate revenue 3–5x. Unlikely in a commoditizing market.

- Dramatically cut CapEx. Surrenders the compute arms race immediately.

- Consolidate or become subsidiaries. This is the likely outcome.

Capital structure flaws drive the pressure rather than operational failure. Hyperscalers sidestep the scaling hurdles currently hobbling standalone firms.

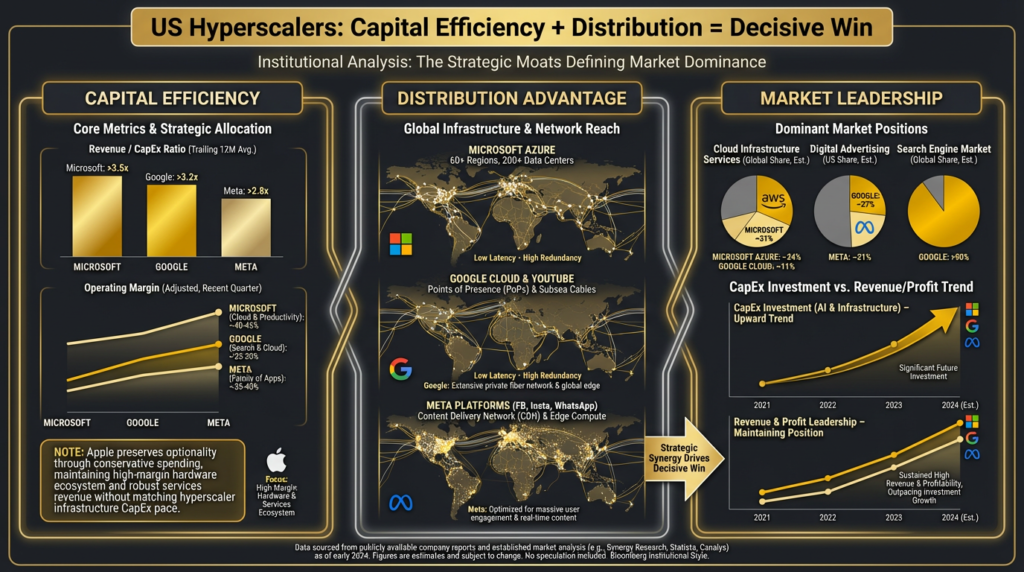

US Hyperscalers: The Structural Moat

Microsoft has already figured out the winning playbook.

The company invested $10 billion in OpenAI not to own a model company but to capture Azure adoption. Azure revenue hit $75 billion in 2025, growing 48%, with AI workloads driving 20–25% of that acceleration. Whether OpenAI consolidates, remains independent, or implodes is almost irrelevant. Microsoft already locked in the margin.

Google does the exact same thing. Google Cloud revenue reached $17.7 billion in Q4 2025, up 48%, powered by enterprise AI migration. The company’s massive CapEx guidance for 2026 is $175–185 billion, nearly double 2025. This isn’t a bet that Gemini becomes an independent $100 billion business. It’s a defensive move: keep enterprise customers from fleeing to Azure.

Meta is more aggressive. Planning $115–135 billion in CapEx for 2026, margins are compressing short-term. But the company has $200+ billion in advertising revenue. That cash flow can absorb the bet because AI enhances ad targeting and recommendation engines. It doesn’t replace them.

Apple takes the efficiency approach. $13 billion CapEx on $250 billion revenue equals a 0.05x ratio. No startup theater, no press releases. Just embedding AI into existing products. Lowest-risk capital allocation in the industry.

The pattern is unmistakable: AI strengthens existing revenue streams. It doesn’t threaten them. That structural advantage (embedding AI into working businesses rather than betting on AI as a standalone product) is permanent. No startup can replicate it.

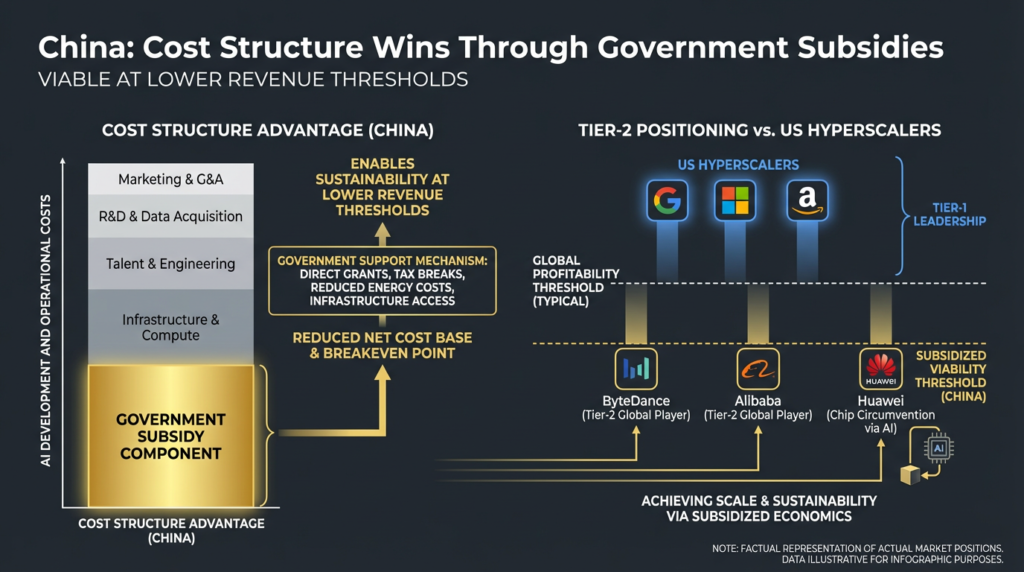

China: Playing A Different Game

China isn’t winning the AI race through superior technology. China is winning through pure capital structure engineering.

Alibaba committed $52 billion to AI infrastructure. ByteDance allocated $23 billion in 2026. These are massive commitments. But the Chinese government embedded financial support throughout the entire system:

Computing power vouchers reduce GPU/TPU access costs by 30–50%. Want to build AI infrastructure in Shanghai instead of Virginia? The math shifts. Electricity subsidies matter because data centers consume massive power. Thirty to 40% of total operating costs go to electricity. State utilities offer preferential rates. Direct capital flows through the $8.2 billion national AI fund plus regional programs, channeling $20–50 billion annually into infrastructure.

The result (per Jefferies Research): Chinese AI models achieve roughly 90% of US performance at 30–40% lower effective CapEx. That’s not innovation. That’s capital structure arbitrage at massive scale.

ByteDance’s efficiency profile proves it. A 0.12x CapEx-to-revenue ratio while maintaining per-user margins higher than Meta. That’s what government-backed infrastructure enables.

As long as China treats AI as strategic infrastructure (which it explicitly does), these subsidies persist. Western competitors lack equivalent policy levers. This gap isn’t closing. It’s permanent structural advantage built into the system.

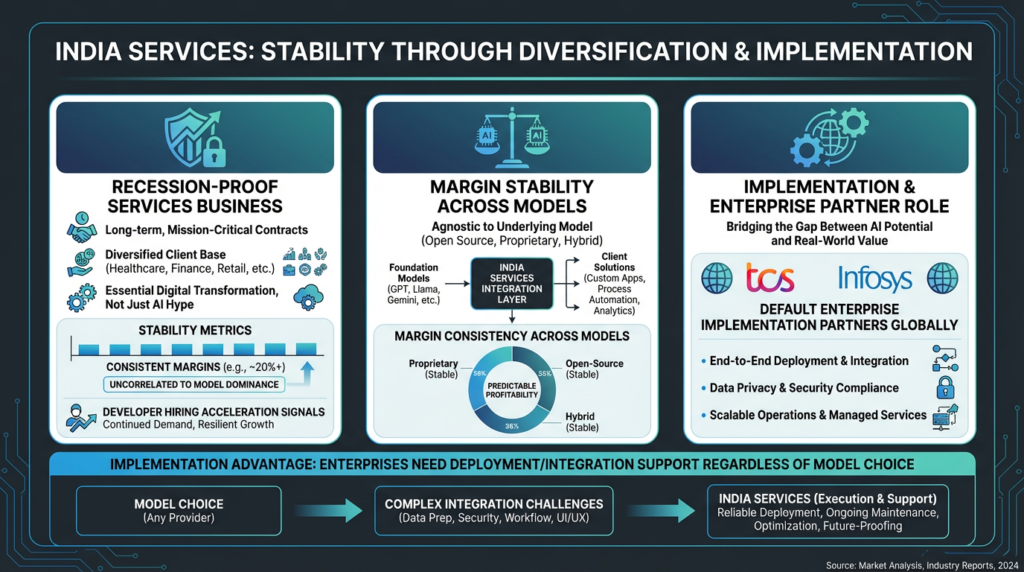

India: The Quiet Winner

While US pure-plays manage cash burn and China builds subsidized infrastructure, India’s AI services firms are executing one of the oldest playbooks in tech: massive labor arbitrage at scale.

TCS reported $1.8 billion in annualized AI services revenue in Q3 FY26 (ending December 2025), growing 17.3% quarter-over-quarter. Infosys sits at $275 million with accelerating growth. HCLTech targets $2.5 billion. None of these companies are betting on proprietary model ownership or building their own infrastructure. They’re doing something far more durable: implementing enterprise AI at 60–70% cost advantage compared to Western consultancies.

The labor math is straightforward. Entry-level AI engineers cost $6–8k annually in India versus $100k+ in the US. Mid-level ML engineers: $12–20k in India, $150k+ in the US. Senior architects: $30–50k in India, $250k+ in the US.

India has 5 million+ AI developers with institutional programs producing more every year. This wage gap is structural, not cyclical. It’s not getting arbitraged away.

The business model is elegant. TCS, Infosys, and HCLTech don’t bet on which AI model wins globally. They win by helping enterprises deploy whatever wins. Fortune 500 companies don’t hire three internal ML engineers to implement Claude or ChatGPT. They contract a TCS team at 60–70% cost advantage compared to hiring internally.

Margin profile: Indian services firms capture 70–75% gross margins on AI implementation. US consultancies capture 35–40% on identical work. That spread is structural, not competitive. The labor cost differential won’t compress.

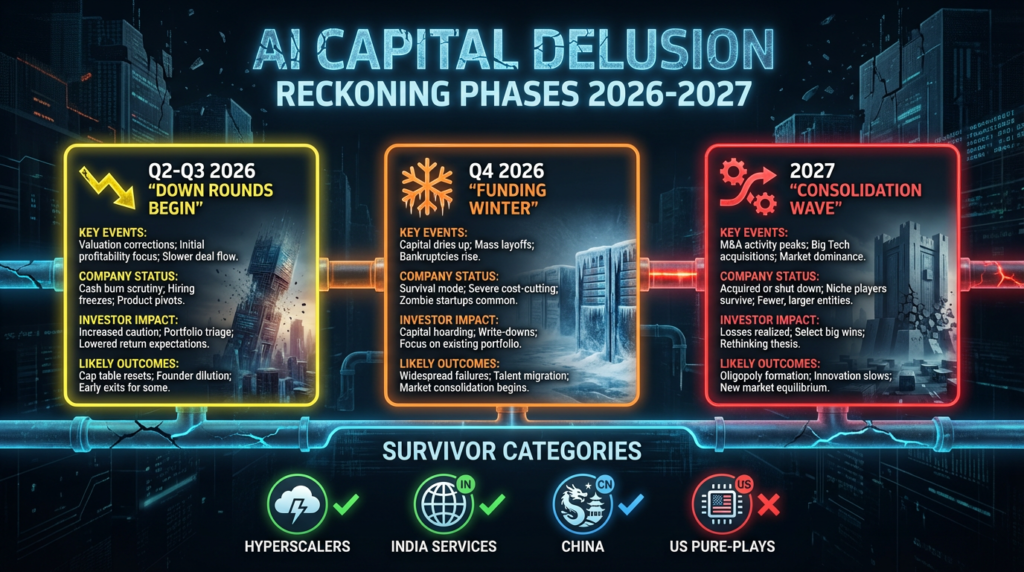

The 2026–2027 Reckoning

The capital pressure cycle will unfold in three distinct phases.

Q2–Q3 2026: Momentum Shifts

Investors flip from “growth at all costs” to “prove ROI or face questions.” Down rounds become common. The narrative transforms from “which model wins?” to “can this company reach profitability?” OpenAI and Anthropic face serious private pressure on runway calculations. This is when the market stops rewarding valuation multiples and starts demanding unit economics.

Q4 2026: Funding Dries Up

Funding evaporates for revenue-less AI startups. Some run out of cash. Consolidation rumors intensify. Hyperscalers begin formal acquisition discussions with pure-plays. Early deals get announced, typically on unfavorable terms for founders and early investors relative to peak valuations. Policymakers start questioning whether AI CapEx actually generates real ROI.

2027: Reorganization

Expect bankruptcies among underfunded startups, distressed acquisitions at 50+ discounts from peak valuations, and forced partnerships. Hyperscalers and India services firms emerge as unambiguous survivors. China maintains efficiency advantage through subsidies. Regional European and Japanese players become acquisition targets or junior partners.

By end of 2027, the landscape looks fundamentally different. Pure-play model companies either consolidate into hyperscalers or operate as majority-owned subsidiaries. Independent pure-play survival becomes rare.

Strategic Implications: Four Capital Models In Competition

The AI industry’s future isn’t determined by technology. It’s determined by who can fund growth sustainably while scaling to profitability.

The Sustainability Gap Is Real: Pure-plays face 1–2 year runways at current burn rates. Hyperscalers face zero capital constraint. China operates at 30–40% cost advantage. India’s arbitrage is permanent.

This Creates Four Distinct Winners:

The reorganization is inevitable. The only question is speed and price.

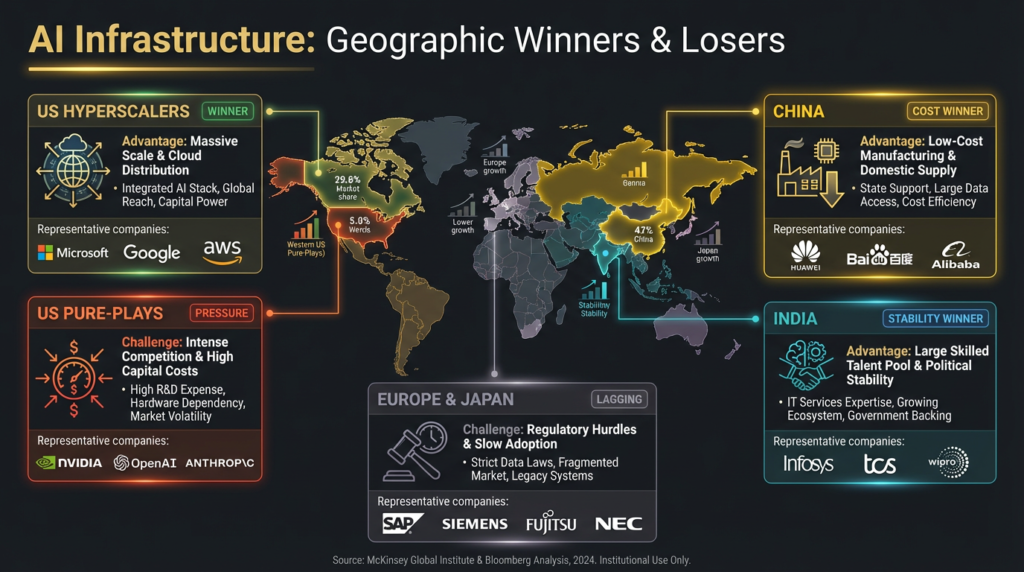

Geographic Winners & Losers

US Hyperscalers: Win decisively. Capital efficiency plus distribution is unbeatable. Microsoft, Google, Meta maintain market leadership despite CapEx surge. Apple preserves optionality through conservative spending.

US Pure-Plays: Face significant near-term pressure as independent entities. Most will consolidate or become subsidiaries. This reflects the business model’s capital structure, not technological failure.

China: Wins on cost structure. Government subsidies make Chinese AI viable at lower revenue thresholds. ByteDance and Alibaba emerge as tier-2 global players. Huawei uses AI to circumvent chip restrictions.

India Services: Wins on stability. Services business is recession-proof, margin-stable, uncorrelated to which model dominates. TCS/Infosys become default enterprise implementation partners globally. Developer hiring accelerates per recent signals.

Europe & Japan: Neither has a hyperscaler with AI distribution, nor subsidies matching China, nor labor arbitrage matching India. Most become acquisition targets or junior partners.

What This Means For Your Capital

For Investors

- Hyperscalers (Microsoft, Google, Meta, Apple): Safest way to play AI. Capital efficiency plus distribution is proven. Near-term margin pressure will stabilize. These stocks reflect AI reality better than pure-play valuations.

- India Services (TCS, Infosys): Expect stable 15%+ AI revenue growth with excellent margins. Uncorrelated to US bubble dynamics. Lower volatility, higher probability of sustained value creation.

- xAI: High-risk/high-reward only if you genuinely believe Elon can force distribution through X and achieve $2B+ revenue. Fundamentally a distribution bet.

- Pure-Play Model Companies: Generally avoid unless they already carry clear acquisition premium pricing. Risk/reward is asymmetric to downside.

For Builders

- Vertical AI Applications: Build industry-specific solutions, not general models. The margin on being the tenth LLM is negative. The margin on legal AI or manufacturing AI is positive and defensible.

- India-Based Teams: For implementation-focused AI, locating core engineering in India is permanent capital structure efficiency. The cost differential won’t compress.

- Partnership Planning: If building a model, assume independence isn’t the exit. Design for integration with Microsoft, Google, or Amazon.

For Policymakers

- Subsidies Work: China’s efficiency advantage is real and embedded in policy. Western governments either match it or accept market share loss.

- Talent Is The Bottleneck: India’s 5M+ AI developers solve the implementation constraint. Talent immigration policy is AI policy.

- Export Controls Have Limits: Chip restrictions slow China but don’t stop it. By 2027, Chinese companies train on domestic chips, reducing US leverage.

The Institutional Phase

What’s emerging now is the AI industry’s institutional phase. The speculative venture-backed period is ending. The consolidation period is beginning.

This mirrors what happened in cloud infrastructure (2010–2015). Winners consolidated around three hyperscalers. Pure-plays either joined them or disappeared. Services firms (Accenture, Deloitte, Capgemini) became the implementation layer.

The AI industry follows the same pattern:

- Consolidation Winners: Hyperscalers absorb pure-plays

- Geographic Winners: China and India emerge as tier-2 players

- Implementation Winners: Services firms capture enterprise deployment

- Losers: Independent pure-plays that can’t reach profitability

The next 18 months separate the serious players from the hype machines.

Chainstreet’s Verdict

The capital sustainability question now dominates everything else.

Winners won’t be the companies with the most impressive demos or the highest valuations. They’ll be the ones with sustainable capital structures and permanent structural advantages:

US hyperscalers win because capital efficiency plus distribution is unbeatable.

China wins on cost structure via subsidies.

India wins on margin stability and labor arbitrage.

US pure-plays consolidate as independent survival becomes difficult.

Geography and capital structure now matter more than raw technology. The next 18 months will separate sustainable players from those facing near-term pressure.

The real AI revolution isn’t happening in model architecture. It’s happening in capital efficiency, geographic arbitrage, and distribution. That’s where the value flows after 2027.

Sources & Attribution

Financial Data:

- Apple 2025 Financial Reports: https://investor.apple.com/sec-filings/

- Google (Alphabet) 2025 10-K & Earnings: https://investor.google/

- Microsoft 2025 10-K & Earnings: https://www.microsoft.com/investor

- Meta 2025 10-K & Earnings: https://investor.fb.com/investor-news/press-releases/

- TCS Q3 FY26 Earnings Report (December 2025): https://www.tcs.com/investor-relations

- Infosys Recent Earnings: https://www.infosys.com/investors

Third-Party Research:

- Jefferies Research (China subsidy impact and effective CapEx reduction estimates): https://www.jefferies.com/research

- Jefferies “Sustaining China AI Competitiveness Through Incentives” analysis

Company Investor Updates:

- OpenAI Investor Updates & SEC Filings: https://openai.com/safety

- Anthropic Investor Communications: https://www.anthropic.com/

- xAI Company Updates: https://x.ai/

Analyst Commentary:

- X Platform (formerly Twitter) Founder Commentary – Q1 2026: https://twitter.com/

- Notable contributors: @aakashgupta, @a16z, @bgurley, @TobiasFrancis, @roshanchandna

Market Data:

- Azure Revenue Growth: Microsoft Q4 FY2025 Earnings Call

- Google Cloud Revenue: Alphabet Q4 2025 Earnings Report

- ByteDance Revenue & Valuation: Industry estimates from Bloomberg, Reuters

- TCS AI Services Revenue: TCS Q3 FY26 Investor Presentation

Estimated Figures Disclosure:

- OpenAI revenue ($4–5B), CapEx ($10B+): Based on investor updates, Bloomberg estimates, and industry reports. Not independently verified by ChainStreet.

- xAI revenue ($0.3B) and CapEx ($5B+): Estimated based on Elon Musk statements, company announcements, and analyst reports. Not independently verified.

- China subsidy impact (30–40% CapEx reduction): Per Jefferies Research analysis and government policy announcements.

ChainStreet Intelligence | Where Code Meets Capital

This report is for informational purposes. Past performance and analyst commentary do not guarantee future results. All financial projections carry significant uncertainty, particularly in markets with high capital volatility.

Activate Intelligence Layer

Institutional-grade structural analysis for this article.